Blog Archives

When headlines are for hire, greed is inevitable

Continuing with the theme of setting each book in a different sector, the Fraudster Series moves to the media industry in the fourth book. Conspirator begins with a hedonistic party thrown by a media mogul in Coorg. Mingling and conniving away from prying eyes and ears, is an intriguing cross-section of powerful men and women – politicians, businessmen, celebrities, and even a blackmailer and a purveyor of fake news.

Things go awry when murder strikes, and very soon, Inspector Dhruvi Kishore finds herself in the bewildering world of fake news, paid new and tailored new.

Be it the west or India, the last year or two have been roiled by fake and disingenuous news. Fake news and dubious social media posts are said to have played a major role in the 2016 US presidential elections. Russia is said to have been involved in it too (Russia has denied the allegation). National boundaries are, of course, meaningless in our digital world.

Closer home, I recently came across a WhatsApp message that seemed to have a particularly malicious intent. The message purported to be a “letter” from a senior director of a global manufacturer of breakfast cereals and snacks to a customer. This purported letter “acknowledged” that the company uses pork and beef gelatin in their products. The malicious message sought to tarnish a global brand in India by taking a leaf out of the Sepoy Mutiny of 1857.

To my horror, I found educated and “enlightened” people forwarding and spreading the message. Even the learned, it appears, fall for such obvious ploys and become unwitting abettors of this insidious mendacity. This is especially so on WhatsApp, where messages can’t be traced back to the originator (unlike Facebook and Twitter).

Clearly, politics is not the only field where fake news rears its ugly head. The business world too is tailor-made for it – tons of money can be made from it. And there are haunts other than politics and business too.

Conspirator distinguishes between three shades of this malaise – fake news, paid news and tailored new. The last is perhaps the most debauched of the three. It happens when trusted journalists (in newspapers, TVs or websites) customise headlines and content to suit private interests – political, commercial or any other. The guardians of truth stoop to cheat and betray the trust they enjoy.

The ones who do this are sly, intelligent people who practice their deceit in a way that makes it difficult for the unsuspecting reader/viewer to realise that what she is reading/watching is tailored news. It sneaks in under her guard and corrupts her perception and beliefs.

Conspirator is the story of such people and their craft. The greatest intangible asset of the media is their ability to influence opinions and choices. The antagonists in the story make use of it to the hilt.

A Wounded Unicorn

As cash crunches strike e-tailers, valuations plummet and down-rounds loom large, the stark reality facing e-commerce unicorns become clear for all to see. Protestations that all is well, and attempts to talk up valuations become less credible by the day. As boardroom conflicts escalate and the day of reckoning fast approaches, a shake-out in the sector becomes imminent. The e-commerce sector becomes a pressure cooker.

Against this backdrop, take a hypothetical e-tailer unicorn that is facing a cash crunch. What if the e-tailer suddenly discovers bugs in its offices and finds that it is the target of corporate espionage? To make matters worse, an investor disappears and a massive data theft follows.

The all-important funding round stalls.

As the stakes escalate and risk surges inexorably, murder follows.

This is the fictional tale narrated in SABOTEUR, the latest corporate thriller set in Bangalore. As bots mimic humans in the Indian cyberspace, men risk millions in Hong Kong. A story of a wounded unicorn and its venture fund investors.

Elephant in the Room – Part 2

The previous post made the case for banks to focus on the proverbial elephant in the room, i.e. fraudulent loans. With loan frauds touching 12% of PSU banks’ net profit, the case cannot be clearer.

Consider the following incidents:

- The stock in a warehouse is pledged for three different loans, and none of the banks knows that the stock is pledged to others.

- A loan is given to ‘ABC Cables’ for factory renovation, but the factory remains shut. The watchman says that the promoter can be found only at the newly refurbished ‘ABC Bar & Restaurant’.

- A property worth 20 crores bears a valuation certificate showing its value as 40 crores.

- An expensive new CNC machine is hypothecated to three different banks, but the machine in reality is a 25-year old fourth-hand wreck.

- The collateral for a loan is stock, but the actual stock is one-fifth of what it is on paper. And the bank doesn’t have keys to the warehouse.

- Newly supplied cartons of computers have only stones and thermocol.

- An auditor certifies the finished goods inventory to be three times the actual inventory.

None of these is of the scale of the alleged Syndicate Bank scam, but few of these, if any, would be unfamiliar to seasoned bankers. It is such frauds, along with some sophisticated ones, that have cost the banking sector Rs. 16,690 crores between 2010 and 2013.

How did this happen? The problem lies as much within banks as in the wider ecosystem, and the weaknesses are both behavioural in nature and systemic.

Basic banking tenets are ignored when operating staff view a bank’s requirements as blind procedures to be followed, or when supervisors pressurise their staff to cut corners. Some are happy to tick the boxes without doing the necessary due diligence. A good part of loan frauds is due to sheer negligence or lack of tools, but another part involves collusion.

While frauds are discovered only when repayment default occurs, their causes lie in weaknesses in the earlier stages of the loan process.

As with any malaise, prevention is better than cure. To do this, we need to improve operating effectiveness within banks, and at the same time, we must implement a central anti-fraud mechanism that can be shared by banks

Improving operational effectiveness

While processes may vary across banks, some key aspects of the loan life cycle are common, and need close attention (see graphic below).

The idea is to make bankers at all levels more accountable and less susceptible to pressure from their bosses. The operating level person who gathers information claims innocence, as he was not the person who had approved the fraudulent loan. At the same time, the bank’s management disclaims responsibility, saying that their decisions are only as good as the information they get. Who then, is responsible? Clearly, it must be both.

According to Deloitte’s Indian banking fraud survey, the top two reasons for frauds are lack of supervision (73%) and pressure to meet targets (50%). This suggests that the management is as responsible as the staff. Unless both are held accountable, provided appropriate tools, and incentivised, it is difficult to see the situation changing.

A bank afflicted by loan frauds must take several steps.

- Firstly, it must commission a fraud risk assessment of the loan process, which will help identify weak areas and take corrective measures.

- Next, it must institute a practice of conducting independent external audits on a random sample of loans. These audits must include surprise physical verification of collaterals, and independent validation of documentation and valuations.

- Third, whenever a fraud occurs, it must trace the histories of colluding employees to identify frauds they may have earlier been perpetrated.

- And finally, it needs to modify employee appraisal systems to bring frauds into focus, and make fraud management central to a bank’s balance scorecard. This must be supplemented with disciplinary action that includes criminal charges.

Even after implementing these steps, the work would only be half done. The other half involves anti-fraud tools.

Do bankers have the necessary tools to detect potential loan frauds? How do they profile loan applicants? How do they inquire into a promoter’s past loan history? How do they know that a collateral is not already pledged elsewhere? For this, we must turn to the second set of actions: implementing a centralised anti-fraud mechanism.

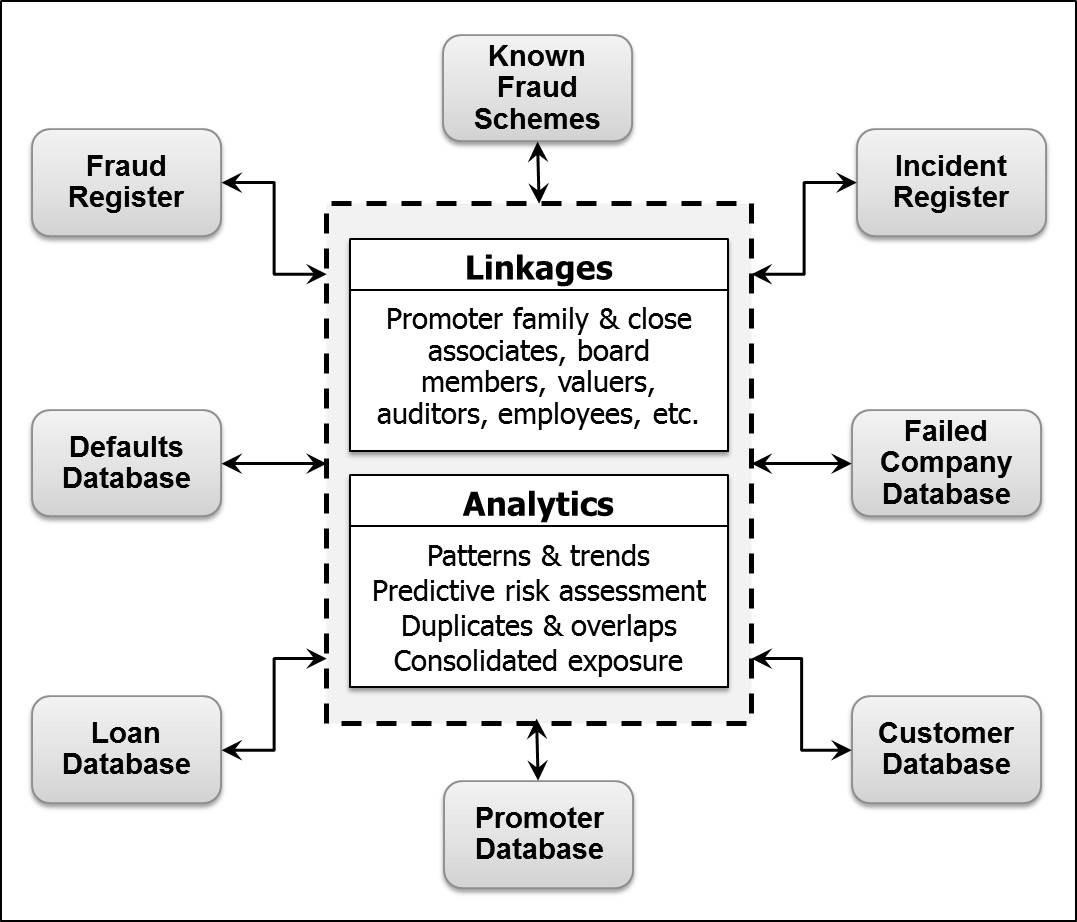

A central anti-fraud system

While RBI has a central fraud monitoring cell, it does not have the necessary tools to prevent frauds. RBI (or some other central agency) must build a centralised system that enables banks to catch potentially fraudulent loans in time by exchanging information on frauds, collaterals, defaults and fraudsters.

Just as a shared claims register helps insurance companies fight duplicate claims, a shared facility will help banks prevent sanctioning fraudulent loans. And if one is sanctioned, it can prevent the disbursal of funds. The central anti-fraud system should have details of all frauds, loans, defaults, defaulters, failed companies, promoters, their close associates, collaterals and fraud schemes. But it must be done in a way that doesn’t compromise the privacy of borrowers.

A promoter or an employee who hits upon a successful fraud scheme is unlikely to stop with one fraud. A shared facility will help nip it in the bud. Similarly, a valuer who overvalues collaterals can be caught sooner rather than later. Wilful defaulters can be pushed out of the banking system.

It is also important to maintain an ‘incident register’ with details of suspicious incidents that are yet to be declared fraudulent. These incidents may be under investigation or under a legal process, but it is critical that other banks are made aware of suspicious activity at the earliest. This incident register must be designed carefully to ensure that privacy and legal rights of customers are not violated. A metadata approach may prove useful in this regard.

The above graphic outlines the concept of a central anti-fraud system. The system must be adaptive, and should be able to flag high-risk promoters, companies and loan applications, after taking into consideration the linkages mentioned in the graphic. In time, it should be able to take in loan application details and give it a risk rating.

Powerful analytic tools are now available, but for them to be effective, they need to be imaginatively combined with an understanding of the fraudster’s methods and the vulnerabilities of our banking systems. Sound design will be key, and the system must have the inbuilt ability to learn on the job. With fraudsters staying a step or two ahead of banks, we will need some sharp minds to participate in this initiative.

There will be those who will seek to thwart the initiative, but the time has come for the banking sector to take some serious steps to fight fraudulent loans.